Webinar on Demand: Combating fraud challenges with data collaboration

Discover how the power of community intelligence can safeguard your business against continuously evolving fraud techniques. At CDQ we believe we are stronger together: tune in and find out, what makes CDQ Fraud Prevention a protective shield that is hard to tear down.

Preventing payment fraud is a complex task. In our recent webinar on the topic, we presented CDQ approach to effective payment fraud resilience. It’s fueled by the vision of data sharing and enabled by ongoing collaboration of industry leaders, who already benefit from the power of community intelligence and are successfully preventing payment fraud for their organizations.

Some basics to get you started

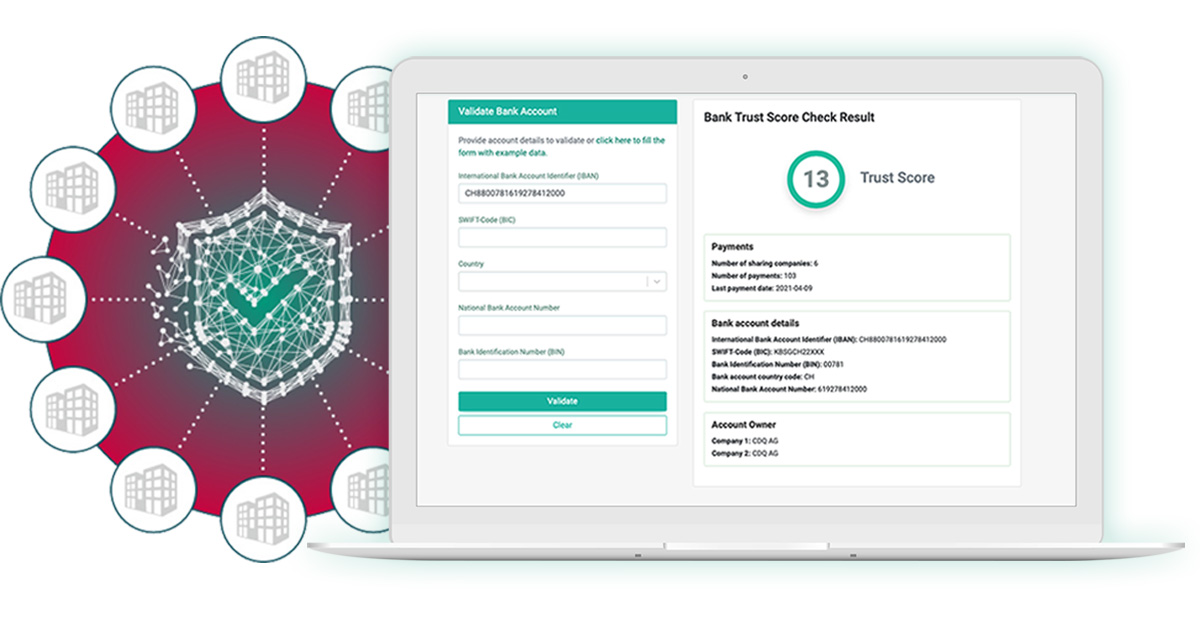

Based on actual statistical use of account data for payment transactions, the CDQ Trust Score helps to quickly check whether given bank account data is known and verified by others and indicated the validity of bank account.

How is CDQ Trust Score calculated?

The score displayed in the whitelist is the sum of individual trust scores assigned by member companies. Each member allocates scoring based on their data in a range from 0 to 3, depending on number of transactions in a given time span:

0: no transactions

1: 1 - 4 transaction

2: 5 - 9 transactions

3: 10 or more transactions

Can I integrate the Bank Trust Score into my internal processes?

Yes, most CDQ customers prefer a solution without any media break. They start using our UI to kick off their Fraud Prevention journey straight away and move towards a seamless API integration.

What about self-affirmation?

If someone in the community does not detect a fraud case and shares the no. of payments within the community? We have a 90 days cooling off period preventing any self-affirmation.

Can I define different thresholds for the Bank Trust Score?

First of all, a trust score of one means that one of our sharing companies has already evaluated the bank account according to a best practice approach. However, depending on your risk level, you can adjust those thresholds. Just get in touch with our sales or customer success team to get more insights.

Can I start off with the UI and change to the API integration or are this two separate services?

Both services are always available for you. As said, usually it’s a journey from the UI towards a seamless API integration. It’s also good to know that we have no user or request limits. So you don’t have to worry about this.

How can CDQ ensure Fraud Prevention, as all is based on historical data?

The history of the bank account proves that it was used for legitimate transactions in a B2B context, while fraudulent bank accounts are mostly private and do not show incoming payments from large organizations. A member company's transactions are only considered if the first payment is older than 90 days, leaving significant time to detect and correct payments to fraudulent accounts.

Are the fraud notifications verified somehow before they are visible to all?

Yes, the fraud notifications need to follow given rules to be published.

In case of any further questions, don't hesitate to contact us and schedule a meeting!

Get our e-mail!

Related blogs

Stepping out of silo thinking: Henkel’s data quality story

A refreshing look at how Henkel tackles an immensely complex data landscape: candid disussion with master data experts, Sandra Feisel and Stefanie Kraft.

The e-invoicing reality: the gateway is ready, but is your data?

Over the past decade, the EU has steadily shifted from encouraging electronic invoices to mandating them. And while the technology obviously plays an important…

A practical guide to managing regulatory compliance in business partner relationships

Regulatory compliance is complex and evolving. Not much of a surprise to anyone in today’s global business environment. Governments and international bodies…